CORSIA Is Here, Supply Is Tight — and Airlines Need to Act Now

By Simon Talling-Smith

Partner, SkiesFifty

The past year has brought absolute clarity on one point: CORSIA is moving ahead, and airlines will face real financial penalties for non-compliance starting in 2027. With the first non-zero Sector GrowthFactor now confirmed by ICAO, and enforcement already embedded in legislation across the EU, UK, Canada and others, the offsetting obligations for international aviation are no longer abstract policy discussions — they are firm, dated requirements. And in addition to a regulatory milestone, CORSIA is also an emerging balance-sheet risk for airlines.

What is less widely recognised is how tight the supply of compliant CORSIA Eligible Emissions Units (EEUs) will be. Only a limited pool of projects currently meets the full Phase 1 criteria, which include updated methodologies, host-country Letters of Approval, corresponding adjustments and revocation insurance. Many developers are still in the process of “upgrading” their projects and are reluctant to make the necessary investments without greater certainty of long-term demand. As things stand, the volume of fully compliant credits expected by 2026–27 is likely to be far smaller than the industry’s collective requirement.

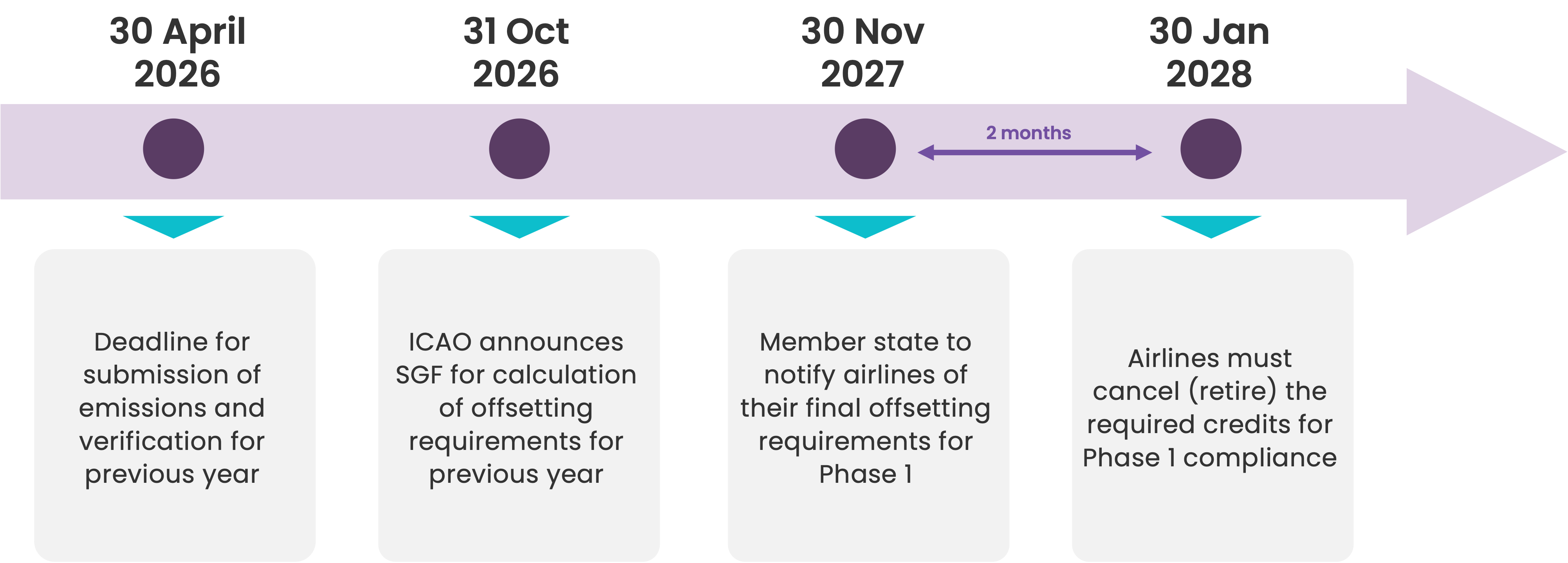

This matters because airlines will receive their final offsetting obligations for Phase 1 in November 2027 and must retire the necessary credits just two months later, by 31 January 2028. Relying on spot purchases during this narrow window exposes airlines to significant price volatility and, in a worst-case scenario, the risk of insufficient supply. With penalties in major markets now set around €100 per tonne, the financial consequences of inaction are substantial.

The experience of other sectors offers useful guidance. Advanced MarketCommitments (AMCs) work because they turn uncertain future demand into an investable signal for suppliers. In the voluntary carbon removals market, the emergence of an AMC — most notably Frontier — provided suppliers with the certainty needed to invest in new capacity, while enabling buyers to secure future volumes at predictable prices. A similar dynamic exists today in CORSIA:fragmented, late-cycle buying will not create the supply the industry needs, nor will it protect airlines from cost escalation by regulators frustrated by inaction.

This is why the idea of a CORSIA Coalition, structured around an AdvancedMarket Commitment (AMC) model, can unlock supplies of CORSIA EEUs. By aggregating demand across multiple airlines, a coalition can lock in multi-year offtake agreements, stimulate suppliers to complete CORSIA-compliant upgrades, encourage host countries to issue LOAs to attract investments, while diversifying exposure across countries and methodologies. Perhaps most importantly, it helps airlines avoid the cliff-edge rush of late-2027 spot buying. Lastly, given the announcement of programs eligible for Phase 2 (2027-2029), airlines and suppliers can now put in place longer term deliveries through to 2031.

CORSIA Phase 1 may seem distant, but the supply chain dynamics mean that 2025 and 2026 are the decisive years. Airlines that act early will secure access, reduce risk and help create a more stable and transparent market. Those that wait may find themselves competing for limited volumes at the worst possible moment.

At SkiesFifty, we see CORSIA not simply as a compliance requirement but as a catalyst for creating a more resilient, investable, and transparent carbon market — one where early, coordinated action gives airlines strategic advantage. The industry has a brief window to take control of its compliance future. Now is the time to use it.